Barnett formula

The Barnett formula is used by the UK Treasury to calculate the annual block grants for the Scottish, Welsh and Northern Irish governments.

What is the Barnett formula?

The Barnett formula is used by the UK Treasury to calculate changes to the funding provided to the Scottish Government, Welsh Government and Northern Ireland Executive, which takes the form of an annual ‘block grant’. It therefore determines the overall funding available for public services such as healthcare and education in the devolved nations.

In 2024/25, the Barnett block grant amounted to £45bn in Scotland, £20bn in Wales and £18bn in Northern Ireland (before adjustments to account for tax devolution). 15 HM Treasury ‘Block Grant Transparency: October 2025, GOV.UK, 9 October 2025), retrieved 10 October 2025, https://www.gov.uk/government/publications/block-grant-transparency-october-2025 This reflects differences in population size as well as the range of devolved public services in each nation.

How did the Barnett formula come into use?

The formula was first introduced ahead of the 1979 general election by the then Labour Chief Secretary to the Treasury, Joel Barnett, whom the formula is named after. It was initially intended as a temporary solution for determining funding allocations between the UK’s nations, but has remained in use.

Until 1999 it was used to determine the level of UK Government spending on public services in Scotland, Wales, and Northern Ireland, and since then it has been used to set the budgets of the devolved administrations.

How does the Barnett formula work?

The Barnett formula calculates changes to the block grants allocated by the Treasury to the devolved governments to fund devolved public services in Scotland, Wales and Northern Ireland.

As originally introduced, the formula was designed to provide the devolved nations the same per capita change in funding as changes in funding for comparable public services in England.

The Barnett formula calculates devolved budgets by using the previous year’s block grant as a starting point (or ‘baseline’), and then adjusts it based on increases or decreases in ‘comparable’ spending per person in England, meaning spending by the UK government on services in England that are devolved to one or more of the other nations. This is defined as the ‘comparability factor’.

Changes to the devolved block grants are calculated by multiplying the change in spending by UK government departments by the comparability factor and the population proportion of each nation.

The basic formula used for Barnett calculations is therefore:

In 2025, the population proportions relative to England were 9.52% for Scotland, 5.49% for Wales and 3.33% for Northern Ireland. 16 HM Treasury, ‘Statement of Funding Policy: Funding the Scottish Government, Welsh Government and Northern Ireland Executive’, June 2025, https://assets.publishing.service.gov.uk/media/684859e3d0ca5d7801e4e6f6/Statement_of_Funding_Policy.pdf

The formula can be applied either to changes in spending on individual services or (at spending reviews) to changes in overall departmental budgets.

At the level of individual services, the comparability percentage is always listed as either 0% (non-devolved) or 100% (devolved).

At the departmental level, comparability factors are on a spectrum ranging from 0% to 100%. A department – such as the Treasury – with a comparability factor of 0% for each of Scotland, Wales and Northern Ireland, delivers all of its services to the whole UK. By contrast, a department – such as the Department for Education – with a comparability percentage of 100% can be understood to be an England-only department, with all its functions devolved to the other nations.

The comparability factor may vary between the three devolved nations, reflecting differences in the devolution settlements.

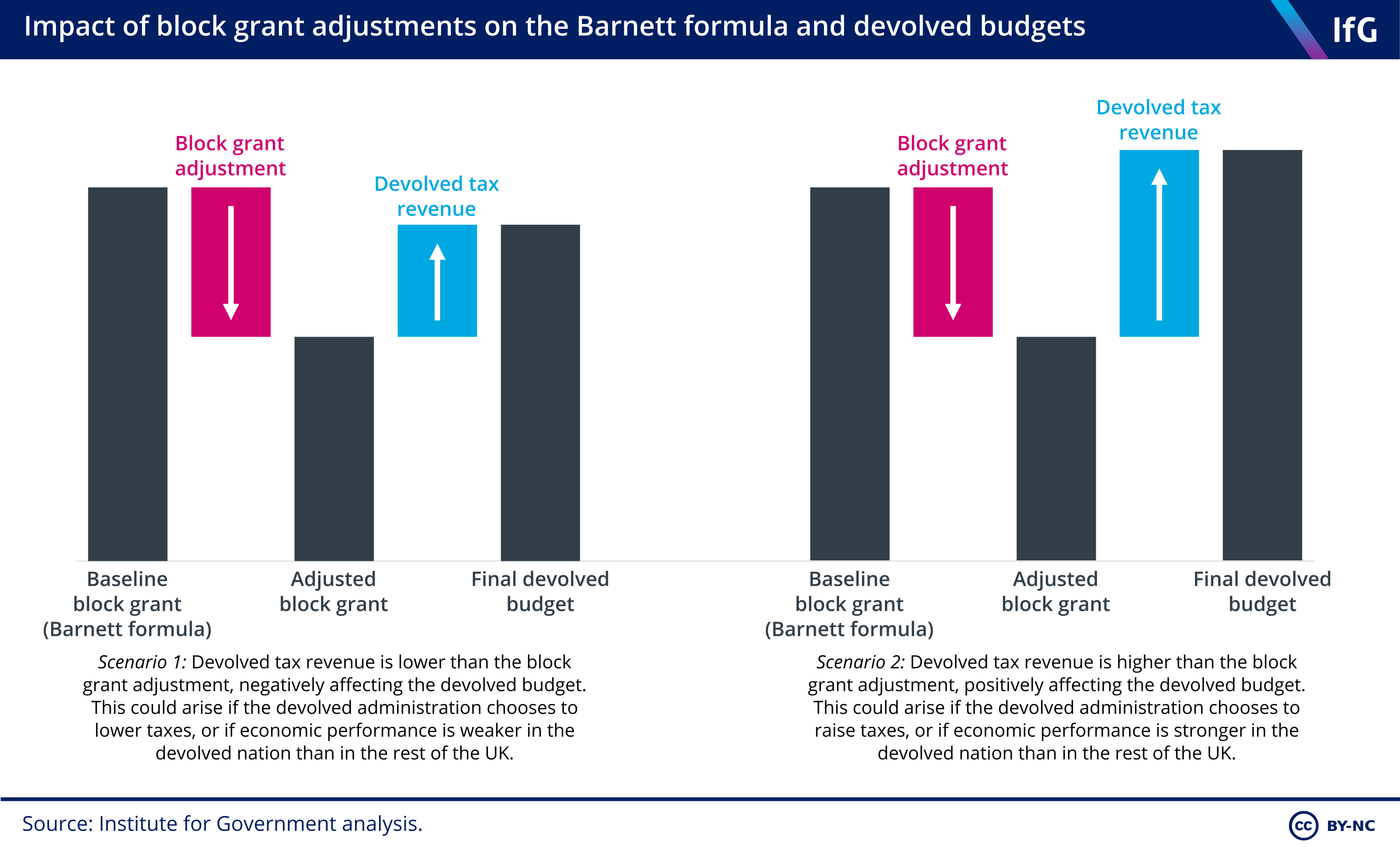

The UK, Scottish and Welsh governments proposed several different approaches for calculating block grant adjustment during tax devolution negotiations in 2016. Eventually, slightly different methods were adopted in Scotland and Wales. In Scotland, the block grant adjustments reflect changes in relative population size, while in Wales block grant adjustments for income tax have been adjusted to account for the fact that Wales has a higher proportion of low earners and would therefore be disproportionately affected by a UK Government decision to increase the tax-free personal allowance.

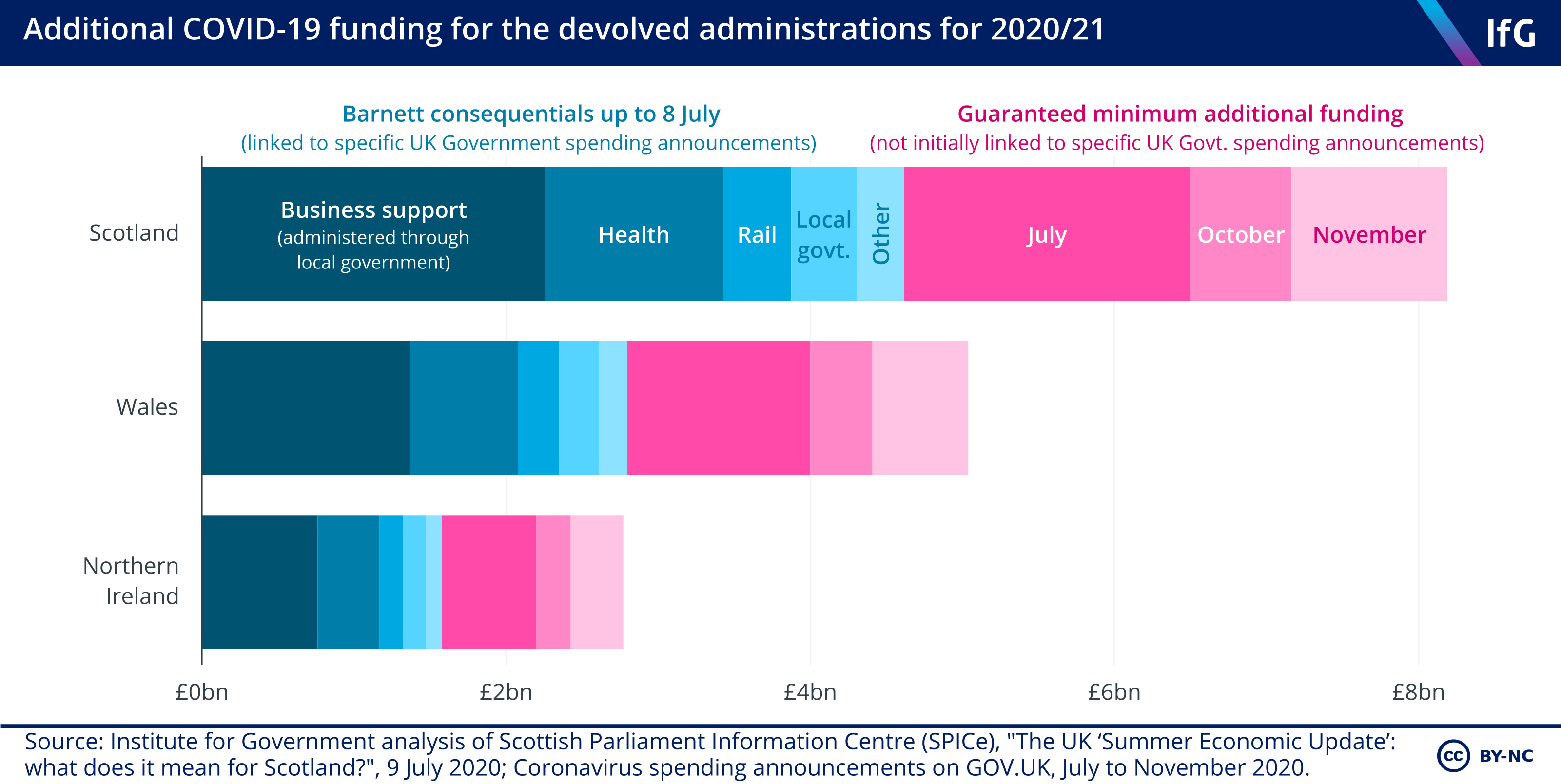

How did the Barnett formula operate during the coronavirus crisis?

The UK Government increased its spending substantially in response to the coronavirus crisis. Some of this additional spending – including on the NHS, public transport and business support schemes – covered England only, resulting in £9bn of additional Barnett funding for the devolved administrations by July 2020.

However, because spending decisions were being taken at short notice in Westminster, and often subject to later revision, the devolved administrations faced uncertainty about their funding. This resulted in the Treasury adopting a new approach for allocating devolved funding in 2020/21. Instead of allocating additional money to the devolved administrations only after new spending was announced for England, the devolved administrations were each given a guaranteed minimum of additional spending to help them respond to the crisis.

Additional spending on UK-wide schemes, such as the Coronavirus Job Retention Scheme (the furlough scheme) did not result in additional devolved funding as the devolved nations benefited from UK government spending on these schemes.