Six things we learned from the 2023 autumn statement

The chancellor presented his autumn statement alongside the latest forecasts from the independent Office for Budget Responsibility.

On 22 November, the chancellor presented his autumn statement alongside the latest forecasts from the independent Office for Budget Responsibility. Ahead of the speech the Institute for Government set out six things it would be looking out for in the speech and documents that were published alongside. Here is our analysis of what we have learned in answer to each of these questions.

Real GDP growth is also lower in every subsequent year of the forecast. This is largely driven by a downgrade in the OBR’s assumption for the trend growth rate of GDP, from 1.8% to 1.6%. This was partly offset by a boost from economic policy – cuts to national insurance contributions, welfare reforms and a package of business support measures including full capital expensing – which increase GDP by around 0.3% in every year of the forecast. Overall, the OBR’s profile for GDP growth is closer to – though still significantly more optimistic than – the Bank of England’s November forecast.

Living standards, as measured by real household disposable income per person, are expected to fall by 3.5% between 2019/20 and 2024/25. This fall is half of what the OBR expected in March (thanks to larger than expected contributions from interest on savings) but is still the largest fall since the 1950s and, perhaps most worrying for Jeremy Hunt and Rishi Sunak, will leave real household disposable income per person lower in the run-up to the next election than in late 2019, when the country last went to the polls.

2. Hunt went for (private sector) growth again

Jeremy Hunt badged his announcements an “autumn statement for growth” and, to an extent, the Office for Budget Responsibility (OBR) agreed with him.

The chancellor announced a package of new tax cuts for business investment (making permanent the previously temporary full expensing policy), cuts to National Insurance contributions and reforms to out of work benefits aimed at incentivising and enabling more people to find work. The OBR estimates that these measures will boost employment by 144,000 and raise economic output by 0.3% in the medium term – a slightly larger impact than the measures he announced in his March budget, which were expected to raise employment by 110,000 and GDP by 0.2%. More significantly, the OBR predicts that the measures on business investment will have an even larger effect in the longer-term.

But this was not an autumn statement for public sector growth. No extra money for government departments, despite higher-than-expected prices and wages, and the tight spending plans beyond the next election were extended for a further year. The OBR cautioned that “reducing the public capital stock as a share of GDP... if sustained… would likely also have a material, negative impact on potential output beyond the forecast horizon”. But, for now, this remains a downside risk which is not reflected in the official economic and fiscal forecasts.

Despite the new policies set out by Hunt, the OBR has downgraded its estimate for growth in the UK’s potential output – from 1.7% a year in March to 1.6% now. This is because the OBR is now more pessimistic about the average number of hours that UK workers will work, the rate at which the UK’s existing capital stock will be retired, and the prospects for productivity improvements.

Autumn statement 2023

What did we learn from Jeremy Hunt's tax and spending plans? See our commentary, podcasts and events on the chancellor's tax and spending plans.

Find out more

Hunt also confirmed spending increases beyond April 2025 of only slightly under 1% in real terms every year, baking in the erosion of real budgets from higher inflation this year and next. The government’s commitment to spending increases on the NHS, defence, foreign aid and childcare implies real terms cuts for unprotected areas of spending: the OBR estimate falls of over 2% per year in real terms. Given rising demand for services – particularly the criminal justice system – that could lead to further substantial decline in performance.

History suggests that whoever forms the next government will likely top up spending when the next spending review arrives, blowing a hole in the current fiscal plans. Low budgets over the next couple of years could prompt further ‘emergency’ funding too, but short-term emergency funding pots, which make it difficult for service leaders to plan effectively and implement productivity enhancing reforms, are poor value for money. The one big public services announcement was on productivity, where Hunt set out a target for 0.5% increase per year. Productivity is an issue in many services – particularly in courts and hospitals – but nothing in the autumn statement will seriously improve the situation. Indeed, the announcement that capital budgets will be held flat in cash terms beyond 2025, which means falling in real terms, will make things worse. Public services will be left with a crumbling estate, insufficient equipment, and inadequate IT systems.

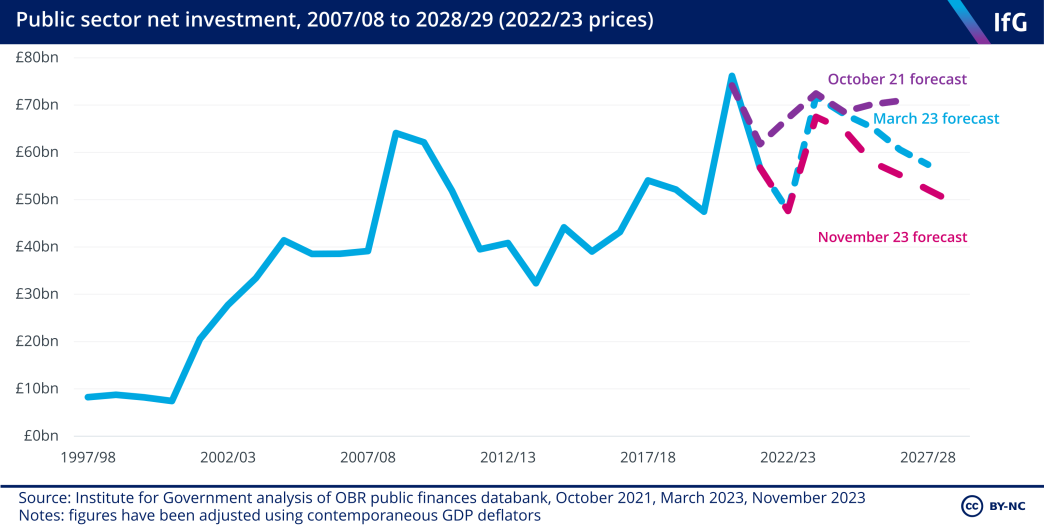

5. Infrastructure received Hunt’s attention but the government’s capital budget was cut in real terms

The chancellor confirmed that government capital spending (CDEL) will remain flat in cash terms from the end of the spending review period. With inflation expected to be higher over the forecast period, this implies a real-terms decrease in the government’s capital budget relative to the March forecast. The OBR forecasts that public sector net investment will fall from 2.6% of GDP in 2023/24 to 1.9% of GDP in 2027/28, compared with the March budget’s forecast of 2.1%. This is well below the target, set at the start of this parliament by Boris Johnson's government, to increase public investment spending to around 3% of national income each year.

While infrastructure did not benefit from any additional public funding (except for some small announcements, such as the space sector), it was still a significant focus of the chancellor’s speech. Hunt’s strategy has been to cut taxes (the introduction of full capital expensing is the most relevant here), reduce regulation and push forward reforms to pension schemes in order to spur greater private sector investment.

The chancellor also announced the government’s responses to the electricity network commissioner’s report 7 Electricity Networks Commissioner’s recommendations, 4 August 2023, www.gov.uk/government/publications/accelerating-electricity-transmission-network-deployment-electricity-network-commissioners-recommendations on reducing the build time for energy projects and the National Infrastructure Commission’s report on planning reforms. 8 //nic.org.uk/studies-reports/national-infrastructure-assessment/second-nia/ The OBR said that these reforms, alongside other announcements, such as those accelerating the consolidation of pension schemes, would likely incentivise additional investment in infrastructure – though did not feel it had enough certainty to quantify the potential benefits.

Infrastructure did not benefit from any additional public funding in the autumn statement.

Under the chancellorships of Sunak and Hunt, the income tax personal allowance, higher rate threshold and (more recently) NICs thresholds have been frozen, rather than being uprated with inflation.