Better borrowing numbers do not mean the chancellor has a tax cuts war-chest

The chancellor and prime minister should not use inflation to cut spending by the back door.

Higher inflation might provide a boost to government tax revenues, but Thomas Pope and Gemma Tetlow warn that it will also make existing – and tight – departmental spending plans appear even less plausible

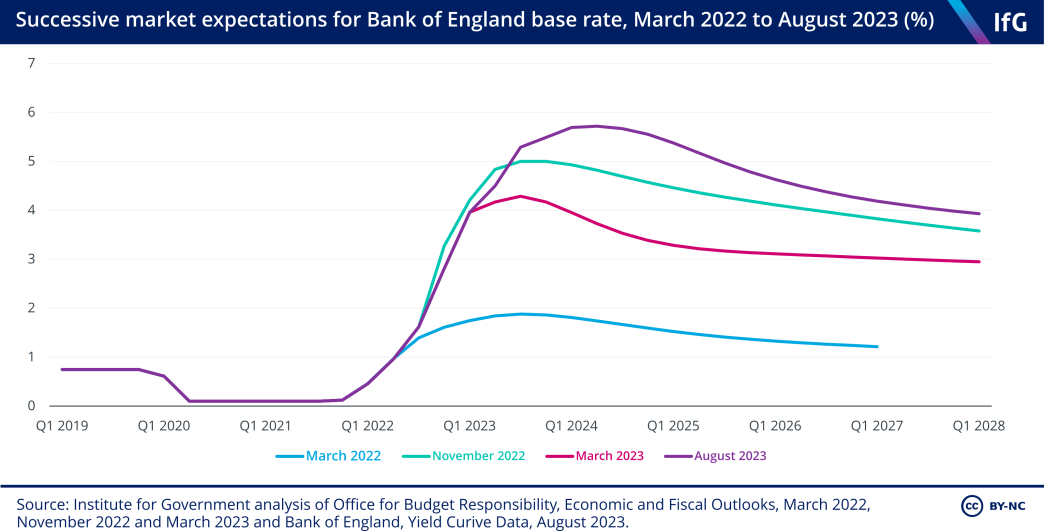

Higher interest rates are bad news for the public finances

One of the main economic developments most people will be aware of since March is a rapid rise in interest rates. The Bank of England’s base rate is now 5.25%, compared with 4% at the time of the budget – a much higher increase than the forecast anticipated back in March when financial markets expected that interest rates would peak at just 4.25%. Instead they have already risen higher and are now expected to stay higher for longer.

This has implications for the government’s spending on debt interest. The rate of interest charged on government debt has increased in line with other interest rates across the economy, so servicing new borrowing is now more expensive. In addition, the Bank of England still holds over £800bn of government debt as part of its Quantitative Easing programme. These are financed at bank rate, so the Bank of England’s decision to raise the base rate has a direct impact on government spending.

Our projections suggest debt interest spending will be at least £15 billion higher than previously forecast in each of the next five years, peaking at an increase of £33 billion next year.

Higher inflation will – superficially – make the fiscal bottom line look better

Since March, there has not been much good economic news. While most forecasters no longer expect a recession this year, most now expect slower growth in 2024 because of higher interest rates, which are designed to cool down the economy. That means overall prospects for real (inflation-adjusted) economic growth look very similar now to what they did in March. 12 HM Treasury, Forecasts for the UK economy: August 2023, GOV.UK, 16 August 2023, www.gov.uk/government/statistics/forecasts-for-the-uk-economy-august-2023

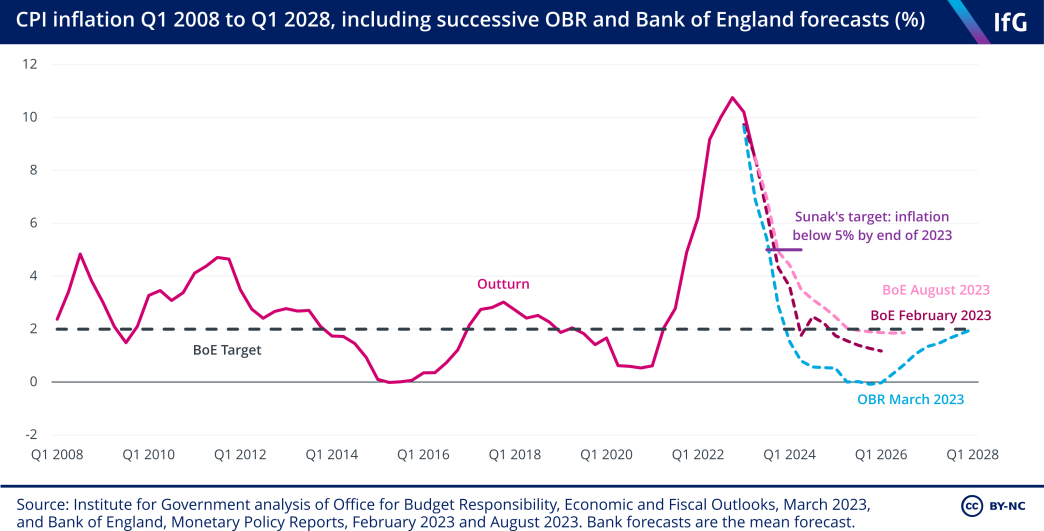

The main change in the outlook is that inflation is now expected to be more persistent. At the start of the year, it appeared Rishi Sunak would comfortably achieve his target of halving inflation by the end of the year (which requires the Consumer Price Index (CPI) to be below 5.0%). But the latest forecasts from the Bank of England now imply it will be touch and go, and inflation is not expected to return to the target level of 2% until 2025.

Inflation has been elevated since early 2022. The initial rise was driven largely by the war in Ukraine pushing up the price of imported goods like food and – most importantly – energy. But as prices went up, incomes did not, so there was no boost in cash tax revenues. At the same time government stepped in with expensive energy support packages, totalling almost £60 billion in 2022/23. The combined effect was borrowing of over £150 billion last year.

However, changes in the outlook for inflation since the start of 2023 are different. Rather than inflation being driven by higher import prices, the reason inflation is now expected to persist for longer is due to domestic factors. In particular, wage increases are averaging around 6%, which is feeding into the price of goods and services those workers produce. This type of inflation still has economic costs, including creating arbitrary winners and losers, which is why the government has a target for low and stable inflation. But it has a different effect on the government’s finances. Wages and spending are now expected to increase more quickly in cash terms, which in turn means faster-growing tax revenues.

Based on how the Bank of England has adjusted its outlook for inflation since March, and assuming this change is driven by domestic rather than imported inflation, increases in tax receipts are likely to more than counteract the fiscal costs of higher interest rates. By the end of the forecast period, when the government’s main fiscal rule applies, we estimate that the government is on course to be borrowing £10 billion less than in March. This positive impact of inflation on revenues is amplified by the government’s current tax policies. Ordinarily, income tax and National Insurance thresholds like the personal allowance increase in line with inflation. But the government has frozen these thresholds until April 2028. That means that faster wage growth pushes more and more of people’s incomes into higher tax brackets.

On the other side of the ledger, some elements of public spending will also automatically increase when inflation goes up – for example, most social security payments (including state pensions and out of work benefits) increase in line with inflation each year. But the largest tranche of government spending – departmental budgets, much of which is spent on public services – are by default fixed in cash terms. So, when inflation goes up, there is no automatic increase.

Domestically generated inflation therefore flatters the government’s bottom line by hiding a cut to departmental spending: fixed cash budgets will stretch less far if inflation is higher.