Six things we learned from budget 2021

We at the Institute for Government had six questions in mind ahead of the budget and this page provides our snap analysis in answer to those questions

As a result of a faster reopening and the effect of the new temporary ‘super-deduction’ boosting business investment, the OBR now expects the economy to recover more quickly than it previously thought.

2. What is the outlook for the recovery?

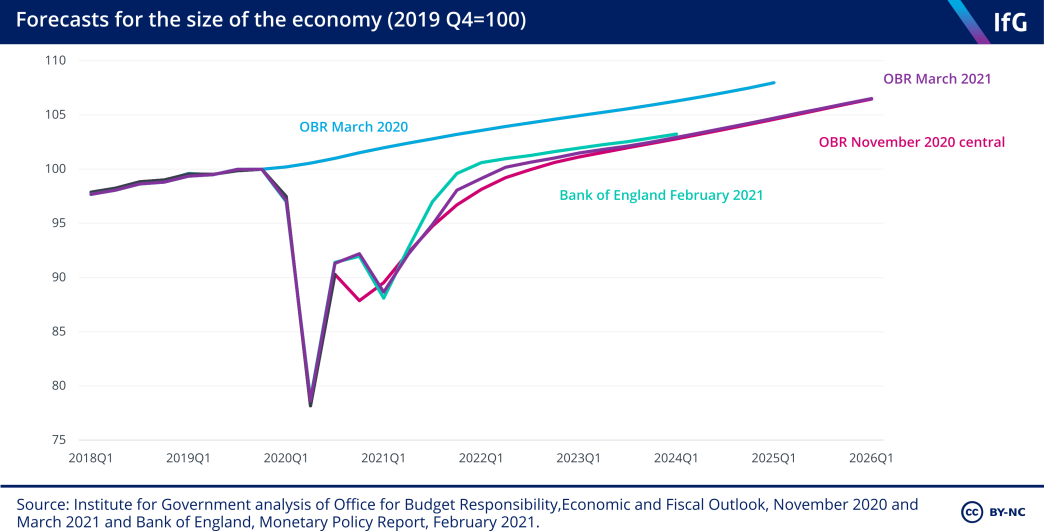

Many will have tuned in to Rishi Sunak’s budget to get a sense of what lies ahead for the UK economy, once restrictions lift and the economy reopens. For this the Office for Budget Responsibility’s (OBR’s) forecast, which accompanies each budget, will have been key.

The economic picture in this latest OBR’s forecast is a complicated one. Since its last forecast, in November, public health restrictions and the prevalence of the coronavirus have been worse than expected. However, the success of the vaccine rollout has also surpassed expectations.

As a result of a faster reopening and the effect of the new temporary ‘super-deduction’ boosting business investment, the OBR now expects the economy to recover more quickly than it previously thought. Rather than reaching its pre-crisis level in early 2023, it now predicts the economy will get there by mid-2022.

However, the OBR does not think this faster bounce back will translate into a fuller economic recovery. It still expects that the economy will be 3% smaller in 2025 than it forecast in March 2020, its last pre-pandemic forecast.

This judgement about the long-term impact of coronavirus on the economy is the most important in the forecast. A smaller economy in the medium term means lower tax revenue and a higher deficit, implying the need for fiscal consolidation at some point. It is also important because it means there is less of a role for stimulus policy in the short term. If coronavirus has done substantial damage to the supply side of the economy, it will not, once the worst of the pandemic has passed and restrictions are eased, be operating significantly below its potential output and so there is little that demand stimulus will achieve except higher inflation.

However, as well as being an important judgement, it is also – as members of the OBR’s Budget Responsibility Committee were keen to stress on Wednesday – an uncertain one, given the unprecedented nature of the Covid shock. We do not know for sure how much damage coronavirus will have done to the economy, and indications of this will only start to emerge once the restrictions lift and the support policies are rolled back.

Despite the rapid bounce back in growth this year and next, then, overall the OBR is relatively gloomy about the prospects of a sustained recovery back to the pre-crisis growth path. We should all hope that this particular forecast judgement is proved too gloomy and the long-term economic damage from Covid is smaller.

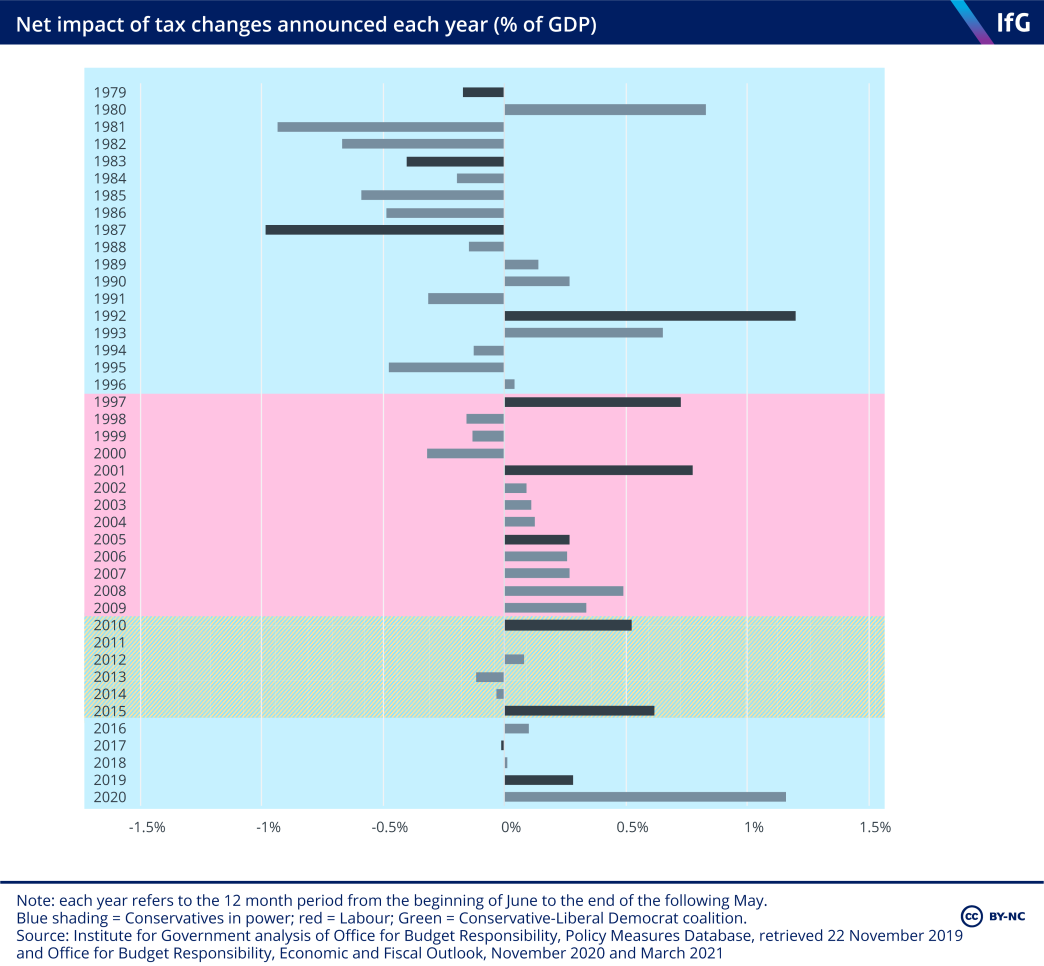

The budget set out substantial tax rises worth 1.1% of national income (or £23bn in today’s terms) which is the largest net tax rise announced in any budget since Norman Lamont’s in 1993.

4. Is fiscal conservatism dead?

The Conservative Party won office in 2019 on a manifesto that pledged not to borrow for day-to-day spending and to leave debt lower at the end of the parliament than the level they inherited – and last autumn, the chancellor told the Conservative Party Conference that “this Conservative government will always balance the books”.

The pandemic blew the chancellor a long way off course but his budget set out substantial tax rises that – based on current economic forecasts – do enough to get him back on track to borrow only for investment by 2025/26. That has been achieved predominantly through a net tax rise worth 1.1% of national income (or £23bn in today’s terms). This is the largest net tax rise announced in any budget since Norman Lamont’s in 1993.

Rishi Sunak said it was too soon to lay out precise new fiscal rules – to replace those originally set by Philip Hammond. But he was clear about what it means to him to be fiscally responsible. He said the state should not pay for everyday public spending, that debt cannot keep rising, and that the government should only borrow to invest. The plans laid out in the budget meet these objectives in the medium term.

The plan for getting there does almost the exact opposite of many of the policies adopted by former Conservative chancellor George Osborne. Sunak is relying almost entirely on tax rises to balance the books, rather than relying on spending cuts as Osborne did after 2010. Furthermore, Sunak’s main tax rises reverse some of the cuts that Osborne introduced: freezing income tax thresholds, after Osborne devoted substantial resources to increasing them faster than inflation; raising the main rate of corporation tax, reversing much of the rate cut that Osborne implemented. The only areas where Sunak has continued in the direction Osborne started are on fuel duty – which continues to be frozen – and the lifetime limit on private pension contributions, also frozen.

The sorts of tax measures that Sunak has deployed are ones that previous Institute work has highlighted as being relatively easy for chancellors to implement – freezing thresholds to allow inflation to drag more of people’s income and assets into higher tax bands, and raising business taxes rather than personal taxes. But he made no mention of some of the more substantive reforms that had previously been trailed – such as tackling the disparity in tax paid by employees, the self-employed and company owner-managers.

Public services were allocated huge sums of money in last year’s spending review to help them respond to coronavirus, but the government did not allocate any new money to them in the budget.

The prime minister has said he wants to secure a “green recovery” but Rishi Sunak’s 2020 budget largely failed to offer signals about how the government would achieve that.