Five things we learnt from the 2020 spending review

Before the spending review, we outlined five things to look for in the chancellor’s announcement. We assess what the statement told us about each one.

1. How will economic performance depend on the path of the virus?

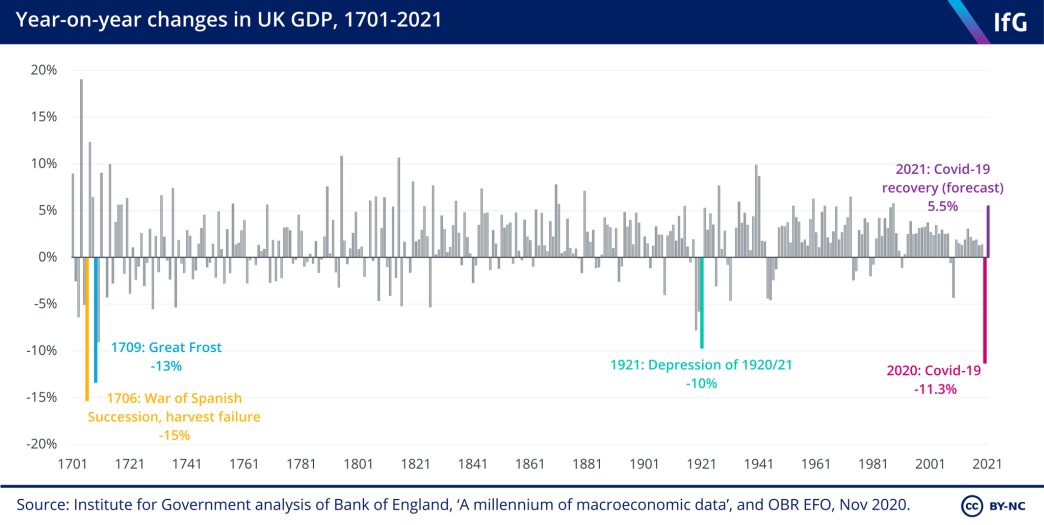

The OBR’s forecast today confirmed what we already expected: the economy will contract sharply in 2020, shrinking more than it has in any year since 1709 (see figure below). The better news is that this is as bad as the OBR thinks it will get. In 2021 and 2022, the economy is expected to grow quickly – by 5.5% and 6.6% respectively in the central forecast. This scenario assumes that a vaccine will be rolled out next year, meaning we can release restrictions in mid-2021.

However, even with this accelerated growth, the economy is only expected to recover to pre-Covid levels at the end of 2022 – and will remain 3% smaller even in 2025 than it would otherwise have been had coronavirus not struck. That means that the virus will have done permanent economic damage even if our lives can get back to normal once a vaccine is rolled out.

In the short term, there may still be some more economic pain to come even as growth picks up. Unemployment is expected to reach 7.5% in the second quarter of 2021 in the central forecast, much higher than the current 5% and only a little below the financial crisis peak of 8.4%. That explains why the chancellor focused so much on a plan for jobs, which he will hope can reduce unemployment more quickly than the OBR’s forecast; it expects unemployment to remain above 5% until the end of 2023.

5. How big is the medium-term hole in the public finances?

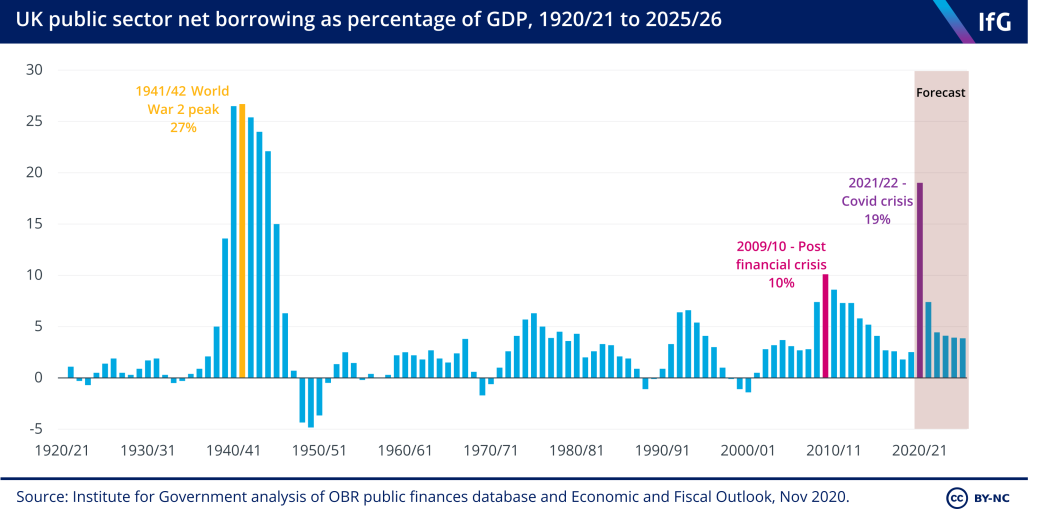

The new OBR estimates of what borrowing will be this year and next (£394bn and £164bn respectively) are staggering by any normal standards. Just eight months ago, the OBR predicted that the government would borrow only £55bn this year and £67bn next.

But more worrying for the chancellor is what today’s OBR forecasts say about borrowing in the medium-term – that is, once the Covid shock has passed and the economy has recovered. On that front, the new forecasts make for even grimmer reading. The OBR now estimates that the UK economy will take a permanent hit from the pandemic – leaving it 3% smaller than was previously expected, even in five years’ time. Borrowing in turn is expected to remain elevated – at 3.9% of GDP in 2025/26. This would be substantially higher than forecast back in March. Since the second world war, the UK has only had borrowing at that sort of level during recessions and their immediate aftermaths.

As Rishi Sunak acknowledged in his speech, the UK could not sustain borrowing at this level for long. He said very little about how he plans to fill this hole in the public finances. For now, the economic and public health imperative is for the chancellor to keep spending. But at some point before the next election, he and the prime minister will have to start laying out what tax rises or spending cuts will be needed to fill this hole and "return to a sustainable fiscal position", as Sunak said on Wednesday is his objective. If the government wants to borrow only for investment (as the fiscal rules set out in the Conservative manifesto would require), the chancellor will need to find net tax rises or spending cuts worth around £25bn a year. More likely £40bn would be needed if he wanted to restore the headroom against this target that he had back in March.