Five things we learned from the spring budget 2024

IfG experts analyse Wednesday's budget announcement

Jeremy Hunt has delivered his latest budget. Our public finances team offer their reaction to the measures announced, and analyse what the new OBR forecasts that accompanied the chancellor's statement tell us about the state of the UK economy.

4. Were spending plans revised, or spelled out?

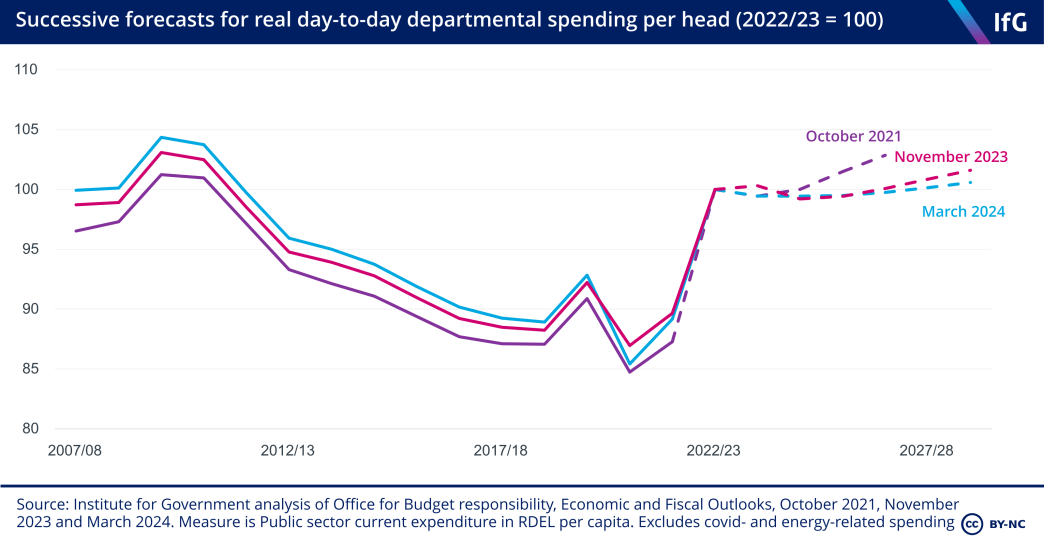

The chancellor has chosen to broadly maintain spending on public services at the same level announced in the autumn statement. For 2024/25, the only major change is an extra £2.5bn for the NHS in England, roughly what the NHS needs to cover the recurrent costs of higher pay deals for staff agreed last year.

The chancellor will need to hope that his tax cuts provide a political dividend, because the 2024/25 spending plans will provide little in the way of good news from public services. Most are performing worse than on the eve of the pandemic and substantially worse than in 2010, and with budgets set to remain flat or fall over the coming year there is little prospect of substantial performance improvements before the election.

NHS waiting lists are projected to start falling from mid-2024 but are likely to still be higher than before the pandemic at the end of the next parliament, while very little progress has been made reducing the case backlog in the crown court. It is also likely that more local authorities could issue section 114 notices, necessitating further painful cuts to services.

The situation from April 2025 onwards is bleak, with real spending per head on unprotected services set to fall by 3.0% per year, down from 2.5% per year in the November forecast as a result of a higher projected population. The reality is that these spending plans will be impossible to deliver. Over the past year, when spending plans were substantially more generous, the government was still forced to provide emergency top ups such as handing around £4bnto the NHS and providing local authorities with £600m more than planned. It has also raided capital budgets to cover shortfalls in day-to-day spending. In total, the government has made in-year cuts to capital budgets of £3.6bn since November.

The chancellor was absolutely right to talk about the potential for productivity improvements – see our recent event showcasing examples from criminal justice services – and some of the investments could make a big difference. However, the promised £3.5bn investment in NHS technology and digital transformation won’t come until 2025/26 onwards, while the impact of cuts to capital budgets in 2023/24 will be felt much sooner. Productivity improvements will be further hampered by ongoing industrial disputes and continuous policy churn.

The government bequeaths a dismal public services legacy to whoever wins the general election. This budget was never going to undo either the short-term effects of the pandemic or the wider problems caused by poor decisions over decades, but the chancellor has done little to set public services on the path to recovery.