Explainer

Adult social care - 10 Key Facts

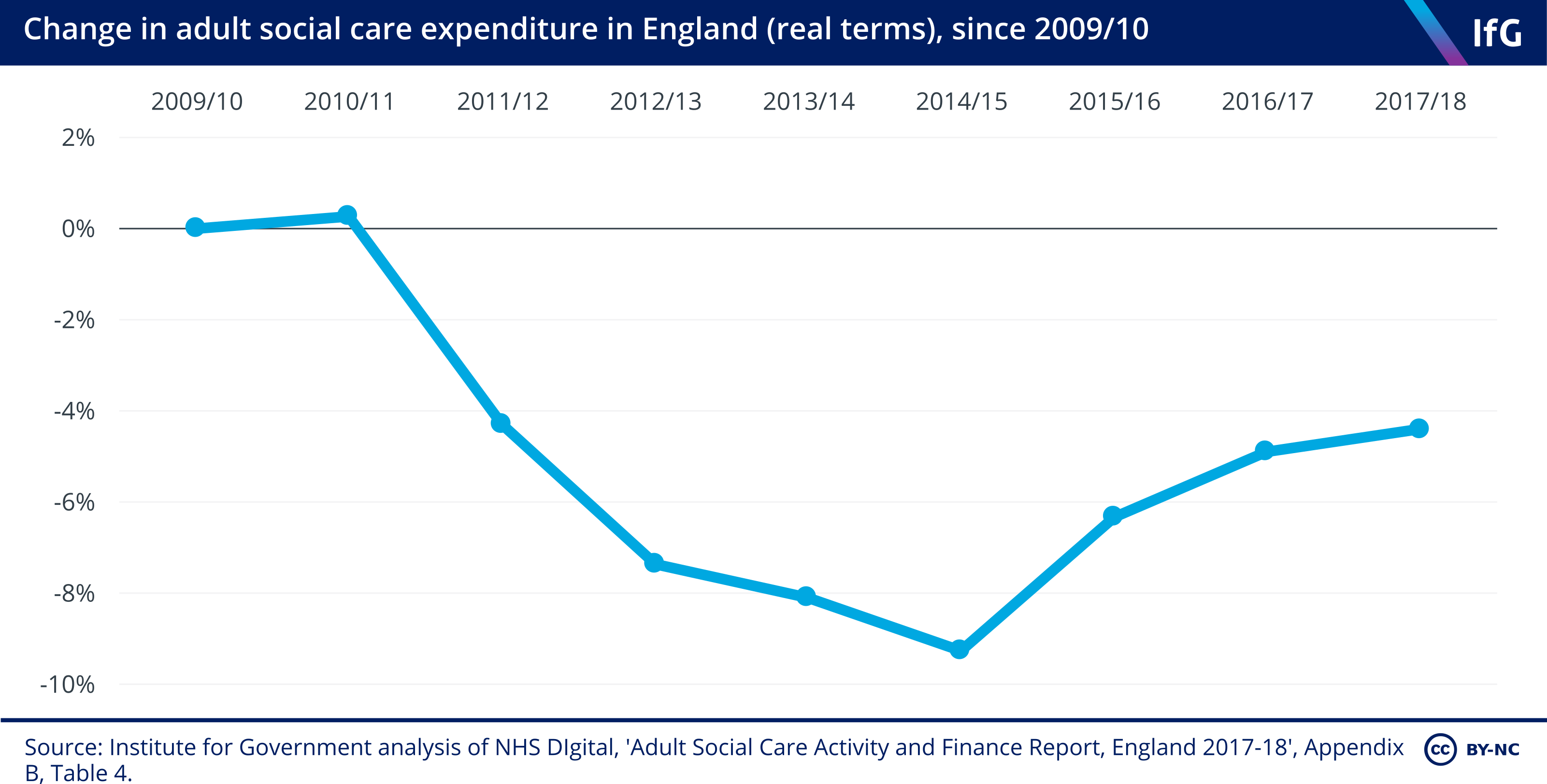

- This followed a period of increased spending. Before 2009/10, there had been an average real-terms annual funding increase since 2001/02 of 5.7%.

2. But spending has increased since then, and will continue to do so.

-

Four new grants and one policy change have led to a slight increase in spending:

- The Improved Better Care Fund announced in the 2015 Spending Review.

- A £2bn top up of the Improved Better Care Fund by 2019/20 in the March 2017 Budget.

- The 2017/18 and 2018/19 Adult Social Care Grants.

- A £240m grant for 2018/19 announced in October 2018.

- The adult social care precept.

- The increased spending is likely to continue. MHCLG estimated that these grants and the precept raised an additional £0.4bn in 2016/17 and £2.3bn in 2017/18, and will raise £3.3bn in 2018/19 and £3.7bn in 2019/20.

- Most analysis suggests there is still a funding gap. The IFS has estimated that the gap between forecast spending in 2019/20 and adult social care need is between £2.8bn and £4bn.

3. Most adult social care is provided outside the public sector.

- In 2018, the NAO estimated that informal and voluntary sector care accounted for most of the value of adult social care (£62bn to £102bn), followed by publicly funded care (£22bn) and self-funded care (£11bn).

- Local authorities have protected their adult social care spending. Adult social care spending made up 36.9% of council-controlled budgets in 2017/18, 34% in 2010/11, and is estimated to rise to 37.8% in 2018/19.

- Local authorities have consistently overspent against planned adult social care budgets. In aggregate, councils spent £132m more than they had budgeted for in 2014/15, rising to £526m in 2016/17. ADASS reported there was no aggregate overspend in 2017/18.

4. The number of people aged over 65 has increased by 19% since 2009/10.

- Older people are more likely to need help. In 2016/17, 43% of people aged over 80 needed help with daily activities, compared with 19% of people aged 65-69.

- The number of over 65s reporting that they need help has decreased. This figure decreased by 1% – just over 26,000 people – between 2011/12 and 2016/17.

- Not all adults in need will seek support. The number of people requesting support has remained broadly flat: rising 2% between 2009/10 and 2013/14, then falling 2% between 2014/15 and 2016/17. This does not mean that demand is flat.

- Yet overall demand has risen. This is because the number of working-age adults with a severe learning disability, mental health problem or physical disability rose by almost 10%. The needs of these groups are often very complex.

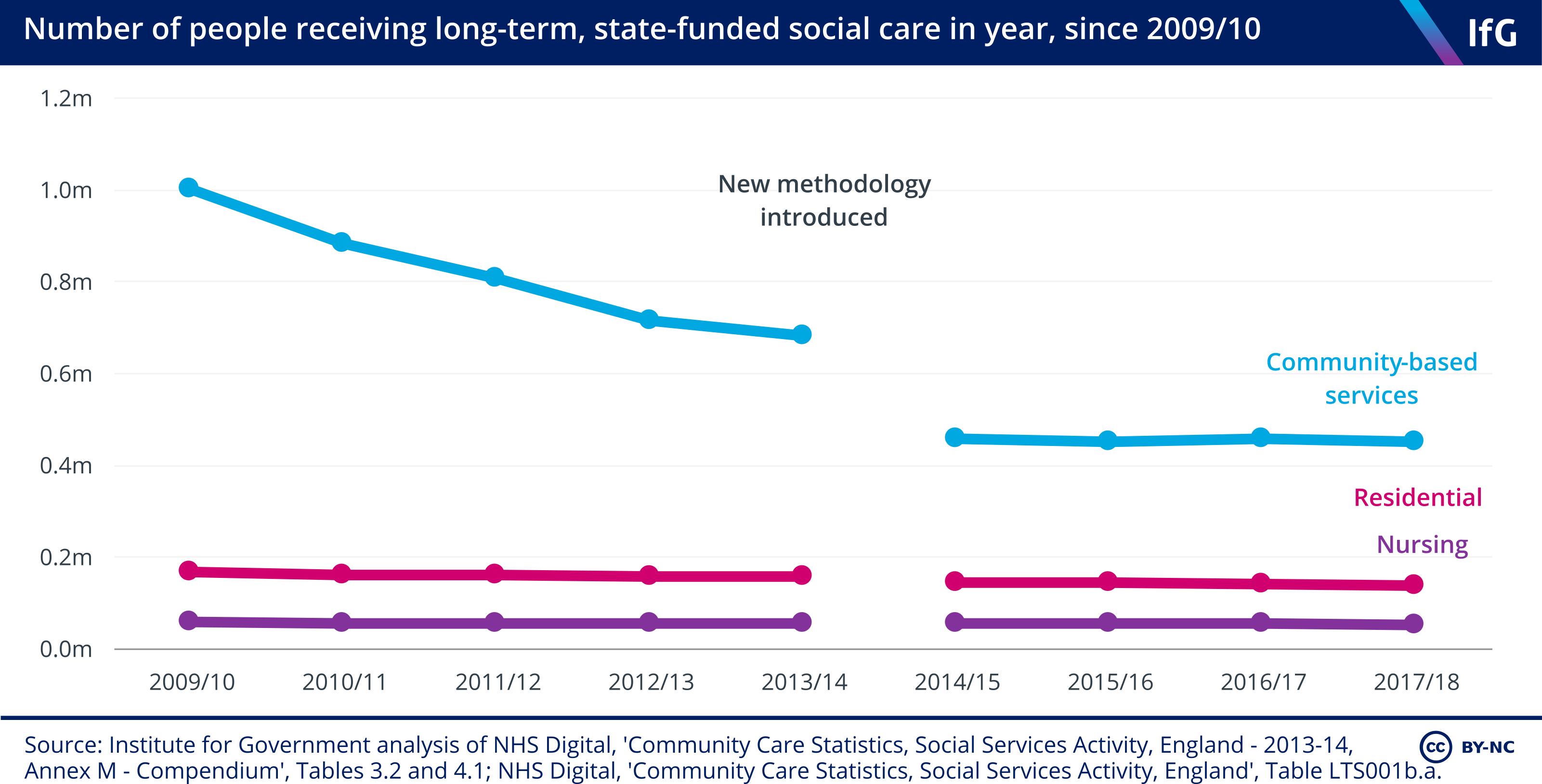

5. The number of adults receiving long-term, publicly-funded social care packages fell by 27% between 2009/10 and 2013/14.

- More intensive and expensive care has fallen by less. Community care packages fell by 32% over the period, but care provided in residential and nursing homes only fell by 6% and 4% respectively.

- This number had previously been increasing. Between 2000/01 and 2008/09, the number of people receiving this kind of care rose by 7.6% (although the data was collected and published differently).

- More people are receiving short-term care. The proportion of adult social care referrals resulting in any kind of short-term care increased from 15.9% in 2014/15 to 17.1% in 2016/17. The number of referrals resulting in re-ablement support rose 2.6% in the same period.

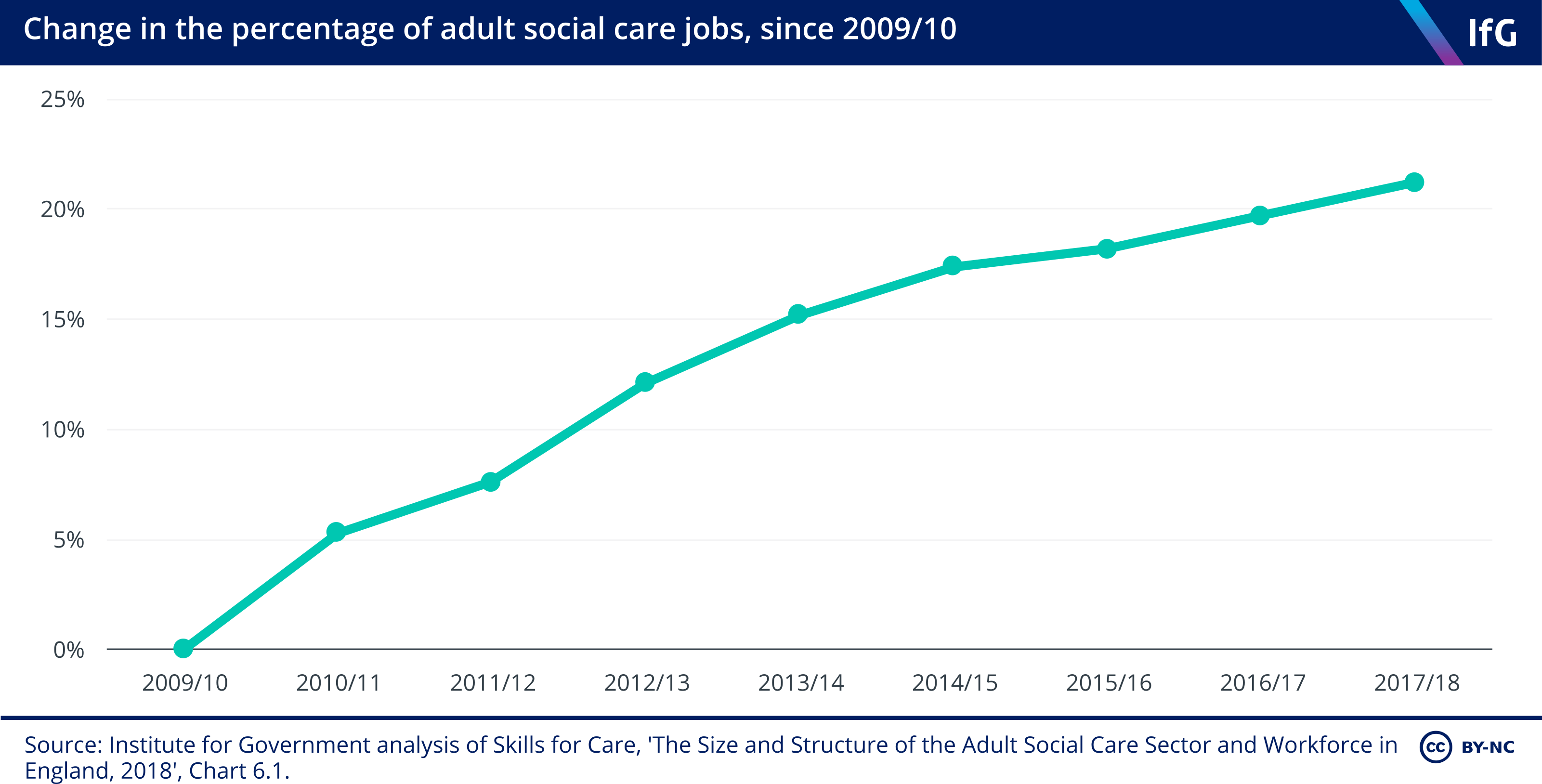

6. There was a 21% increase in the number of adult social care jobs between 2009/10 and 2017/18.

- The social care workforce in England is growing. However, some of these jobs are part-time, and multiple jobs may be held by a single person.

- The composition of those jobs has changed. The number of jobs in the independent sector increased by 28% between 2009/10 and 2017/18, while the number of jobs working directly for local authorities fell by 39% due to service closures and outsourcing.

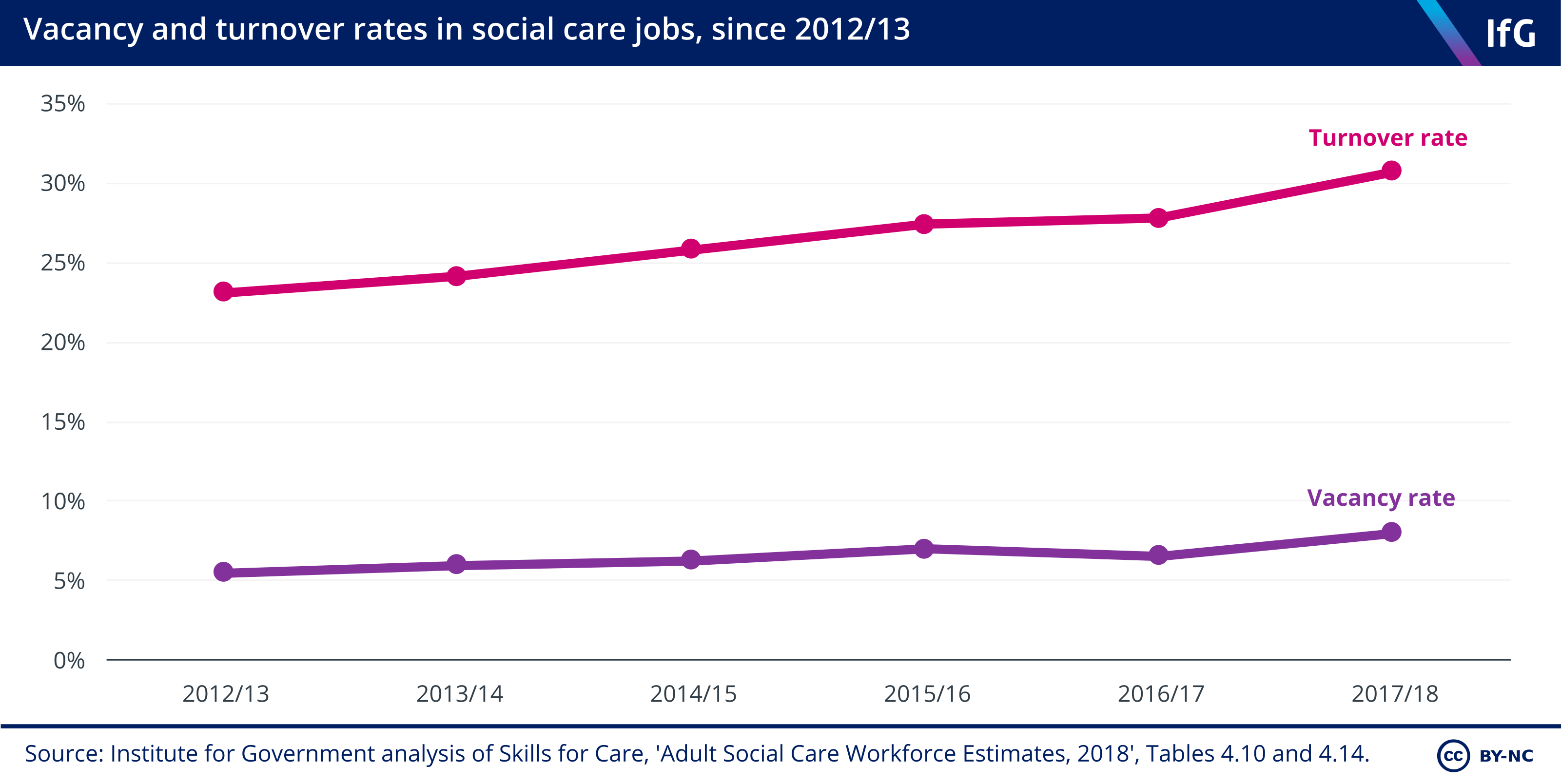

7. In 2017/18, 8% of all social care jobs were vacant, and the turnover rate of social care staff was over 30%.

- The vacancy rate in direct care is higher. Here, the vacancy rate increased from 6.4% to 8.6% between 2012/13 and 2017/18. The largest vacancy rates were among social workers (10.8%), occupational therapists (9.8%) and care workers (7.7%).

- Turnover has increased too. Between 2012/13 and 2017/18, social worker turnover rose by 5.0%, care worker turnover by 9.1% and registered nurse turnover by 5.2%.

- Some of this turnover is internal. In 2017/18, 40% of leavers left for another job within the adult social care sector, and 67% of new starters were recruited from within the sector.

8. Between 2010/11 and 2013/14, the fees paid by local authorities to residential and nursing care providers fell by 9% in real terms.

- This put real pressure on providers. Since 2009/10, care homes with a greater share of local authority-funded clients have consistently made economic losses of between 2% and 8%. The CMA estimates that local authorities are paying approximately 10% below the total cost of care home places.

- The same is happening in home care. In 2016, the average hourly price that English councils paid for home care was £14.66; only 10% of all councils paid the estimated minimum sustainable price of £16.70.

- Local authorities are seeing home care contracts handed back. Between 2016 and 2018, 40% of councils had a home care contract handed back.

- This is not sustainable. Due to pressures from increased staff costs, two-thirds of councils increased provider fees between 2014/15 and 2015/16, and more than 60% of councils increased residential, nursing and home care fees by more than 3% in 2018.

9. Between 2016 and 2018, the share of all care providers that the CQC rated as 'outstanding' and 'good' increased by 19% respectively.

- Those receiving care have not seen a drop in quality (based on limited evidence). The proportion of care providers rated ‘requires improvement’ or ‘inadequate’ declined by 14% and 6% respectively.

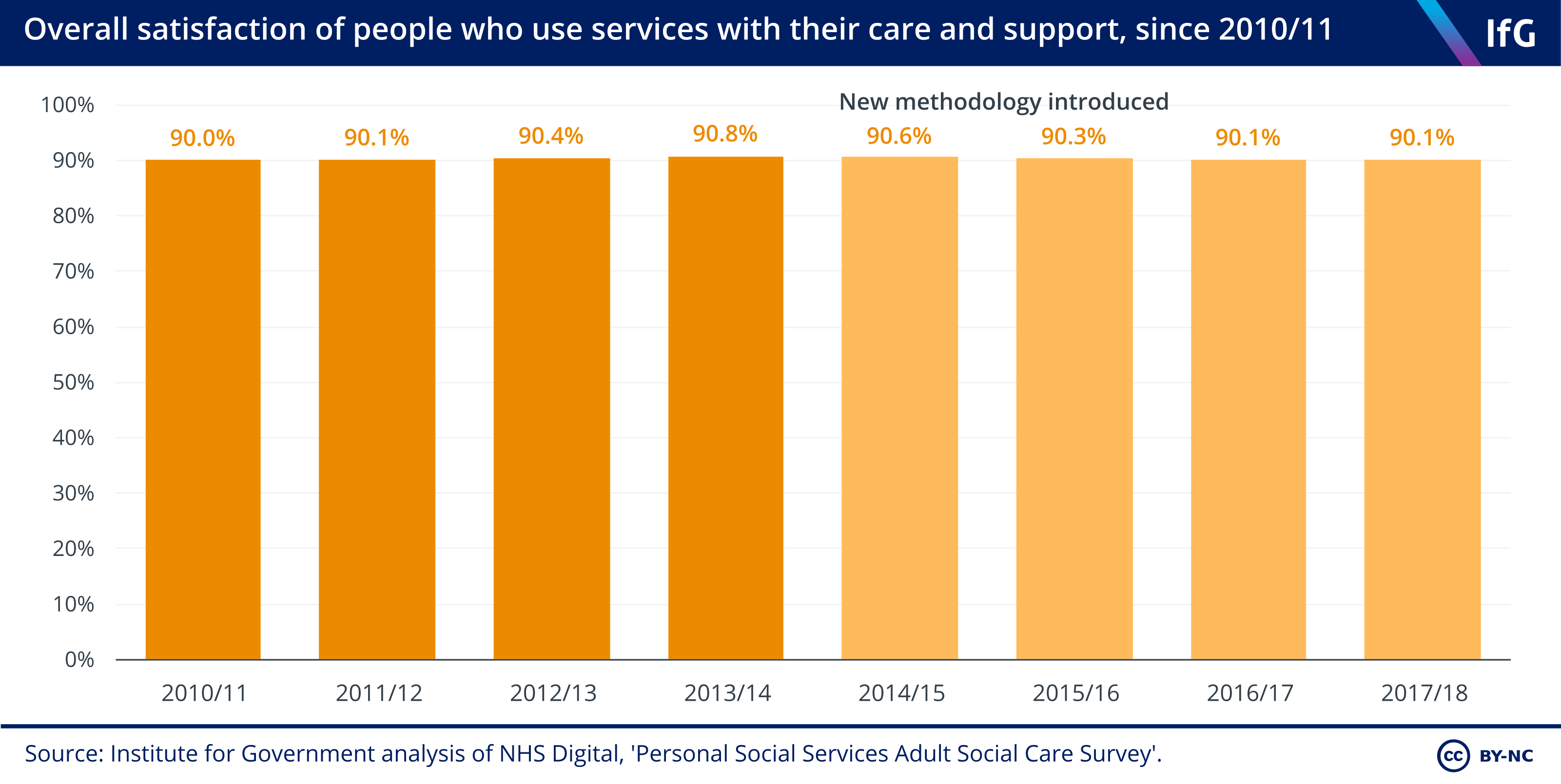

- Satisfaction has remained high among users of social care services. The number of social care users who say they are ‘very’, ‘extremely’ or ‘quite satisfied’ has remained between 90% and 91% since 2009/10.

10. On an average day in 2017/18, 1,900 hospital beds in England were occupied by someone whose discharge was delayed due to social care.

- In 2016/17, it was even higher – almost 2,500.

- Since March 2017, delays due to social care have declined rapidly. But they still remain higher than in 2010.

- Most delayed transfers are due to patients waiting for a care package in their own home. This rose from 12,777 days in August 2010 to 33,520 days in March 2017 (an increase of over 160%).

- More people are receiving unpaid care. The ONS estimates that the number of people receiving continuous care in the UK (168 hours a week) grew 14.3% between 2009/10 and 2014/15. There was a 16.4% increase in hours of unpaid care between 2009/10 and 2013/14 from 7.3bn to 8.5bn. This has since declined to 7.9bn in 2016/17.

- The value of unpaid care has increased. The amount it would cost to purchase care currently provided informally increased consistently after 2009/10, but declined slightly from £68.7bn to £68.3bn between 2015/16 and 2016/17.