Brexit dividend

This explainer sets out how any Brexit dividend (or otherwise) is reflected in the government’s official independent forecasts prepared by the OBR.

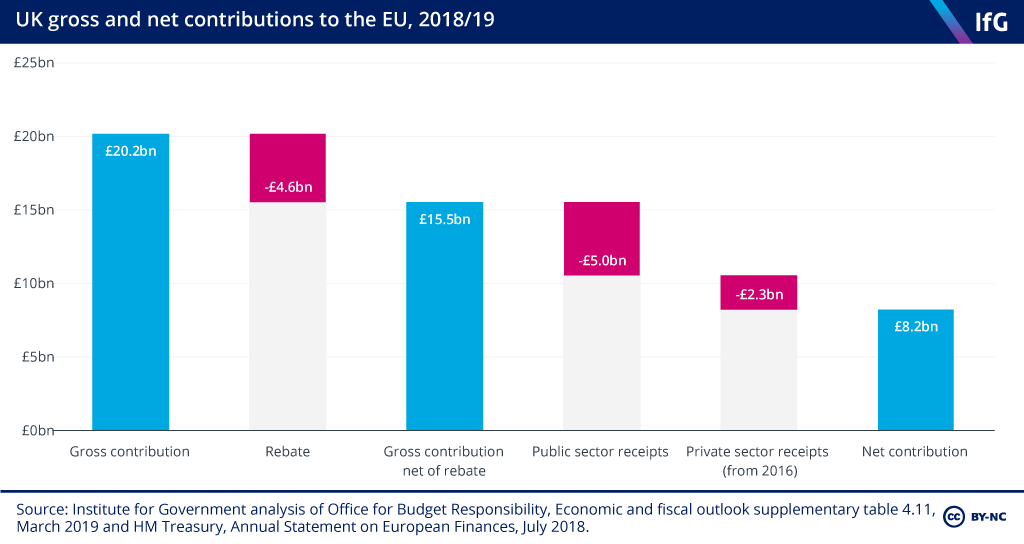

Over the next few years, under the terms of the Withdrawal Agreement, the UK will continue to make payments to the EU in respect of commitments made before it left (for example, ongoing pension liabilities). These payments are largest over the next few years – €7.5bn (£6.3bn) in 2021, declining to €1.3bn (£1.1bn) in 2024 – then are negligible beyond the mid-2020s.

In previous forecasts, the OBR has assumed that all ended EU contributions would be recycled into other (unspecified) spending. In fact, the government could replace all spending from the EU in the UK, such as farm subsidies, and still have an amount equal to £8–9bn per year (in 2020 prices) from the mid-2020s left over.

Tariff revenues

Part of the UK’s contributions to the EU are the tariff revenues collected by the UK as part of the customs union, collected when goods enter the EU single market via the UK. In 2020/21, the UK collected tariffs worth £3.4bn, and the EU provided a rebate of £0.7bn (notionally to cover the cost of collecting those tariffs). These tariff revenues contribute £2.7bn of the £8–9bn net contribution set out above.

The UK is leaving the EU customs union, which means that it will no longer collect tariff revenues on behalf of the trading bloc. In future, the UK will set its own tariff regime, and patterns of trade will change. If the UK sets higher tariffs – including imposing tariffs on EU trade – it could raise more in revenue than the £3.4bn currently collected. If, on the other hand, the UK adopts lower tariffs than the EU – at the extreme adopting ‘unilateral free trade’ and imposing no tariffs at all – tariff revenue could be very low.

Deciding on how to approach tariffs highlights the tension between the government’s focus on the direct and indirect public finance impacts. A punitive (high) tariff regime would mean more revenue is raised on goods at the point of entry; this is a direct financial impact. But doing so would likely mean lower economic growth as it would make the UK a less open economy (as discussed above). It would likely cause other indirect revenues to fall and the deficit to rise too, and so would result in a negative wider economic impact.

Overall assessment

An estimate of the negative economic impact has already been factored into the official forecasts, but the upside – from no longer making EU contributions – is not, as that money is currently floating around as ‘unallocated’ spending in the fiscal forecasts.

That said, while the economic effects are uncertain, forecasts suggest that a negative indirect impact from lower economic growth would outweigh any positive direct impact of the UK no longer paying contributions into the EU budget or setting its own tariffs. It is, then, unlikely that there the UK is to enjoy any meaningful ‘Brexit dividend’.