Five things we learnt from Jeremy Hunt's 2022 autumn statement

The IfG team give their verdict on the chancellor's autumn statement and what it means for government borrowing, households and public services.

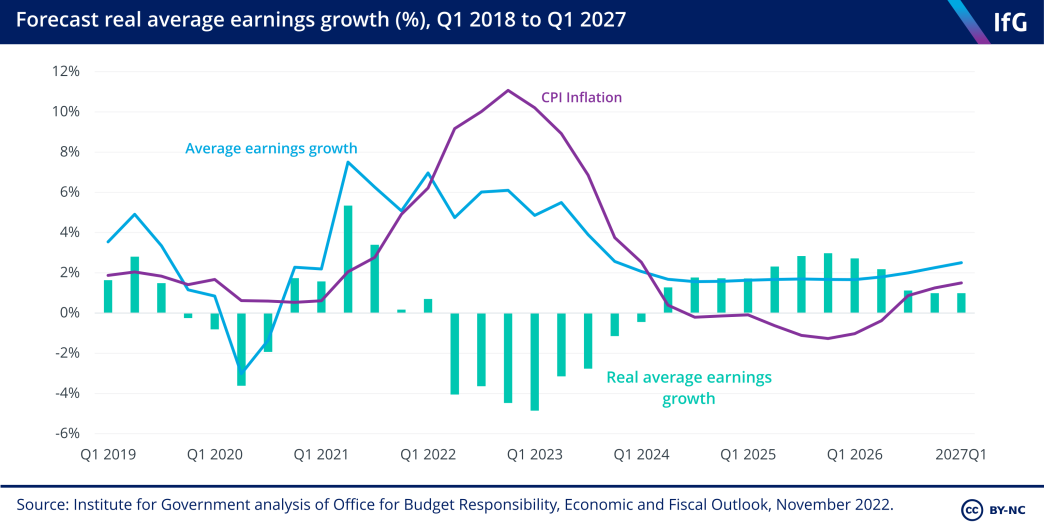

The Office for Budget Responsibility (OBR) expects real household disposable income (a measure of living standards) to fall by 7.1% between 2021/22 and 2023/24.

2. How much worse is the economic and fiscal outlook?

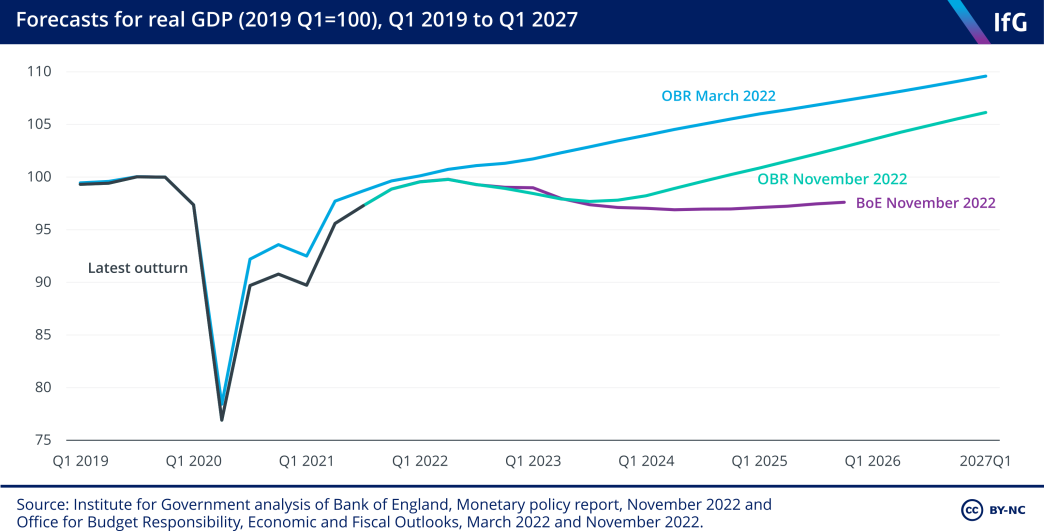

The economic outlook has worsened substantially since the Office for Budget Responsibility (OBR) published its last forecast in March. Back then the OBR predicted that economic growth would slow next year, after the post-pandemic rebound in 2021 and 2022, but continue to be around 2% a year. But since then it has become clear that the UK is headed for recession, as the global energy crisis has intensified, inflation has risen faster and the Bank of England has hiked interest rates more quickly than previously anticipated.

The new OBR forecast is for the economy to contract by 1.4% in 2023, before growing sluggishly in 2024 and then more strongly in 2025 and 2026. This is a substantially weaker path for growth than the OBR expected in March. It puts the OBR roughly in the middle of the pack among UK economic forecasters but is notably more optimistic than the growth forecast published by the Bank of England just two weeks ago.

This weaker economic outlook translates into weaker public finances. Tax revenues are expected to come in less strongly as the economy is weaker, and the government will come under pressure to spend more on debt interest payments and benefits in response to higher interest rates and higher inflation. In the absence of any policy action in the autumn statement, higher debt interest costs would have added £52.7bn a year to borrowing by 2027/28. Other adverse changes to the economic forecast would have added a further £29.3bn, giving a total of £82.1bn higher annual borrowing by the end of the forecast horizon.

Jeremy Hunt responded to this downgrade to the medium-term economic and fiscal picture by announcing tax rises and spending cuts. Taken together, all the policy changes that have been announced since March will save the exchequer £38.8bn a year in the medium term.

The net effect is to leave the government on course to borrow 2.4% of national income in the medium term. This compares to a plan for medium-term borrowing of just 1.1% of national income back in March.

The Bank of England has hiked interest rates more quickly than previously anticipated.

3. What are the government’s objectives for debt and borrowing?

Jeremy Hunt today announced the latest set of fiscal rules, the ninth set of rules in the last 15 years. As has been the case previously, a new set of rules was adopted largely because the old ones were due to be missed – this time because of the large deterioration in the economy.

While Rishi Sunak’s primary fiscal rule required that debt be on course to fall in the third year of the forecast (2025/26 for the autumn statement), Hunt’s rule only requires debt be on course to fall in the fifth year (2027/28). This represents a notable loosening of the rules and allows the government to reduce the deficit more slowly than would otherwise have been the case. The government is on course to meet this target, though only with around £9 billion of headroom to spare – compared to the roughly £30 billion of headroom that Sunak had against his rule in March.

Hunt’s other rule is that borrowing should be less than 3% of GDP in the fifth year of the forecast. It is welcome that the government has an additional rule on borrowing as well as debt, because debt rules can be easy to manipulate. However, while recent governments have had a rule requiring that the government be on course to run a current budget surplus (borrowing only to invest), Hunt’s rule makes no such distinction between day-to-day and capital spending.

There is a good rationale for a current budget rule – in other words, one that specifically restricts the level of day-to-day spending relative to government revenues, while allowing additional borrowing for investment. This is because capital spending (such as investment in infrastructure) is more likely than day-to-day spending to benefit future generations who will be required to pay back any borrowing.

Historically, investment spending has been an easy target for governments seeking spending cuts as it is politically easier in the short term, with costs only emerging in the long term. Hunt has followed this course – achieving 40% of his spending cuts in the autumn statement by holding capital spending fixed in cash terms from 2025, albeit investment spending (at 2.2% of national income by 2027/28) will still be relatively high as a share of national income by historical UK standards.

Overall, in historical terms these are a permissive set of rules. In only six previous forecasts has the Office for Budget Responsibility projected a current budget deficit in the fifth year of the forecast horizon.

Despite the permissive nature of the current rules, the scale of the economic downgrade since March means that meeting these rules has nonetheless required tricky decisions on tax and spending. And Hunt has left only a small margin for error against the rules, meaning any further deterioration of the forecast could necessitate additional action next year.

Energy profits levy will increase from 25 to 35% from 1 January and there will be a new temporary 45% levy on electricity generators.

Health, social care and education received a combined additional £9 billion in day-to-day funding in 2024/25.