Six things we learnt from the spring budget 2023

What the chancellor's announcement revealed about the government's plans for tax and spending policy.

On 15 March 2023, chancellor Jeremy Hunt presented his first budget. This set out the government’s plans for tax and spending policy. Alongside it, the Office for Budget Responsibility (OBR) published updated economic and fiscal forecasts for the next five years – running up to and beyond the next election. Here are six things we at the Institute for Government learnt from the chancellor’s announcement.

The chancellor used some of this fiscal space in the near term to keep the energy price guarantee limit at £2,500 per year for the average household.

The OBR has forecast that the UK’s GDP will be higher than previously expected at the end of the forecast.

Jeremy Hunt's measures on spending increases and tax cuts have left the chancellor with just £6.5bn of headroom against his main fiscal rule on debt.

4. Will the government address pressures on public service workforce and performance?

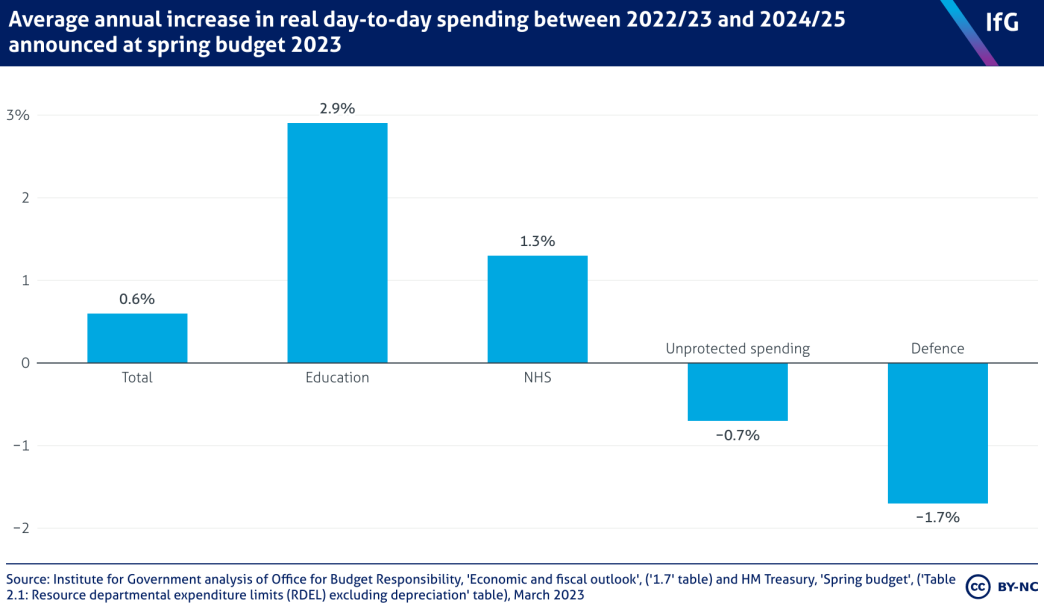

Despite speaking for over an hour the chancellor managed to avoid talking much about public services at all. Given the large number of public sector strikes this week, including on budget day itself, and the bad state of many public services highlighted by the Institute for Government and CIPFA’s Performance Tracker 2023, this was a notable omission.

He left departments’ spending totals mostly unchanged, though he did find extra money for defence and his new childcare commitments. That means most services will see only small budget increases over the next two years, with even tighter plans still pencilled in beyond the current spending review period, from April 2025 onwards – that is, after the next election.

These tight budgets could undermine Hunt’s ambitions to promote growth: the OBR rightly cautions that “additional resources” will be needed to deliver the chancellor’s growth-enhancing measures like the new disability employment programme. 9 https://obr.uk/docs/dlm_uploads/OBR-EFO-March-2023_Web_Accessible.pdf , p23

A major cause of the current problems in public services is that many – most notably the NHS – are operating less productively than before the pandemic: even where budgets are increasing, they are not translating into better results. Yet there was nothing in this budget to address that, and the eagerly awaited NHS workforce plan – which Hunt announced in November – was not released either.

Hunt did not address strikes during his speech. But his decision to maintain departments’ existing budgets will also make it very hard for departments to offer pay increases large enough to match those in the private sector – which could cost £11 billion, according the OBR – and so bring an end to ongoing industrial action.

10

https://obr.uk/docs/dlm_uploads/OBR-EFO-March-2023_Web_Accessible.pdf, p99

However, the chancellor has retained a larger-than-usual reserve (unallocated departmental spending) of over £13 billion in each of the next two years. This is ‘dry powder’ Hunt could deploy to make more generous pay offers later. That he increased the overall spending envelope to pay for his new defence commitments, rather than taking it from this reserve, suggests that he wanted to retain that flexibility.

The notable omission from Hunt’s long speech was much discussion of public services.

The chancellor was silent on public sector capital spending plans.

Jeremy Hunt announced a series of big tax giveaways in the budget, including a permanent increase in the generosity of pensions tax allowance.